Company Overview

Going to skip this one. If you don't know Nintendo you are not from this planet.

|

| (click chart to enlarge) |

Analysis of Operation

|

| (click chart to enlarge) |

|

| (click chart to enlarge) |

Regular readers will have figured out that I am more inclined to concentrate on the asset and the cash flow side in my analysis. I don't do any predictions about where sales, margins, EPS, etc. could be in the next quarter or next fiscal year. I am pretty agnostic about future profitability (as long as I expect that some profits will materialise). The main reason is, that it isn't really my circle of competence. Furthermore, I am convinced that if I get the margin of safety on the asset side right my results should be satisfactorily.

If you are interested about where Nintendo has come from and where it might be in the future operationally, I recommend you watch an excellent presentation by Steven Towns at last years Value Conference, which is to be found here:

http://www.valueconferences.com/2012/page/10/

In 2004 Nintendo introduced its handheld device DS. It's interesting to note that the DS launch didn't materialise in an expansion of Nintendo's overall sales figures. But it did materially so in an expansion of its profit margins. Especially net-income margin expanded from 6,4% in FY2003 to a whooping 18% in FY2006. Apparently the DS product was highly profitable.

With the introduction of the Wii console Nintendo's sales saw an astounding boost.

Along with it margins, especially operating margins, expanded significantly to almost 30%. Interesting to note is that net margins couldn't keep pace with operating margins. Basically the net-margin didn't increase sustainably at all and kept oscilating around 15%.The reason is mainly to be found in two prevailing conditions during that time:

Firstly , sales increased faster than did the (stated) net-income.

Secondly, currency gains (especially against the Euro) between 2003-2007, which ended up in a ridicolous overvaluation of the yen, kind of boosted Nintendo's operating margins "artificially". After the launch of the Wii depreciation of the yen started to flatten out, with a resulting mitigating effect on Nintendo's net results.

|

| (click chart to enlarge) |

EPS saw an incredible run from a low of of ¥ 234 in FY 2003 to an astounding ¥ 2000 in FY 2008.

Average EPS (15yrs.) is ¥ 800 ==> average P/E of 12 at todays stockprice.

ROE and ROA averaging a very healthy 11% and 8%.

With the financial crisis, and the rapid strengthening of the yen against all major crosses, Nintendo's margins crashed as spectecular as had been the run up. In FY 2011 Nintendo had to post its first annual loss of ¥ 60 bln.in 30 years.

|

| (click chart to enlarge) |

Maybe more interesting than the WiiU console in itself for future sales might be the network strategy Nintendo is introducing with the console launch. Here especially I find the video on demand strategy quite appealing, as content is as important (or even more so) than hardware.

Analysis of Cash-Flow

|

| (click chart to enlarge) |

The introduction of the DS and Wii did also materialise in operating cash-flow readings and FCF readings.

Both metrics expanded significantly. Due to the fact that Nintendo's businessmodell is very capital light, expansion of operating cash- flow translates almost fully into free cash-flow.

The huge loss in FY2011 pushed the operating cash- flow disproportionaly high (to net-loss) into negative territory. The drainag of valuable cash resources is pretty shocking. I urge readers to investigate that fact. And please let me know when you have come up with a sound argument why this might be so! (I know the reason, but it is incomprehensible to me why Nintendo would do that).

Average OCF (15 yrs.) is ¥ 870 ==> P/OCF of 11. Interesting is to see that at Nintendo there is no material divergence between OCF and earnings. This is mainly attributable to the abscence of excessive depreciation.

Having said that I have to caution the reader (and encourage) to investigate the last three fiscal years regarding depreciation politics.

Average FCF (15yrs.) is ¥ 462 ==> an average FCF yield of more than decent 8,5%

|

| (click chart to enlarge) |

Analysis of Balance Sheet

Nintendo is debt free. Given that it has got only little personal, its pension obligations (although in a deficit) are nothing to write home about. Thus, overall liabilities are negligible and represent only 13% of total assets.

Current Assets/ Current Liabilities

.png) | ||

| (click chart to enlarge) |

Although Nintendo is not a Graham net-net stock (which would be obscene), Nintendo's valuation on a NCAV and net-net basis is ridicolous (given the strong franchise of the company).

The premium of present market capitalisation to NCAV isn't even 50%! With cash making up almost the entire current assets balance.

|

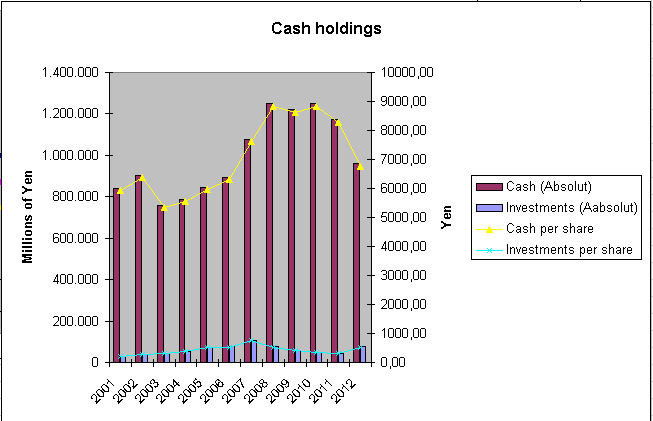

| (click chart to enlarge) |

Unfortunately cash holdings got quite a significant beating in the last fiscal year due to the aforementioned huge hit to operating cash-flow.

|

| (click chart to enlarge) |

Current ratio and acid test (=current assets ex. inventory) always has been rock solid, but are awe- inspiring in the last two fiscal years. Main factor is a radical cut back in current liabilities. To be frank about Nintentdo's current asset position (as so many japanese stocks) it is extremely overcapatilised.

Book Value

Nintendo is trading rougly at stated book value. This has to be regarded as cheap having in mind the historical earning power the stock has shown and the strong franchise of the brand.

Overall asset composition is very favourable too, with PP&E and cash&short term investments representing the biggest chunk.

|

| (click chart to enlarge) |

Prior to the reversion of the earning trend (FY2010) and last FY's loss, Nintendo had constantly increased its retained earnings for 13years. During 1999-2010 it increased its net-assets on average by 6,5% p.a.

In the last two years it has lost roughly 10% of its net-assets.

|

| (click chart to enlarge) |

BPS growth would have been even more impressive than net-asset growth, if I had included significant share buybacks Nintendo undertook in the last 15 years. Given that Nintendo (unfortunately) didn't retire those shares I refrained from substracting treasury shares from total shares outstanding due to conservatism in my valuation approach.

Analysis of Pay-out Policy

Policy on profit distribution is rather complicated at Nintendo. Basically it is a percentage of net-income.

I find it a little bit disturbing as Nintendo is so cash rich. It would be more shareholder friendly if Nintendo introduced a fix component of dividend.

|

| (click chart to enlarge) |

|

| (click chart to enlarge) |

|

| (click chart to enlarge) |

At least Nintendo didn't slash the dividend entirely due to the loss they posted in FY 2011.

Although Nintendo engaged in stock repurchases in the past, they didn't do so in recent history.

That is quite of a shame, as buying at those distressed shareprice level would very likely put a floor under the stock. Furthermore it would benefit the stockholders who are willing to hold on to the stock significantly should things turn for the better operationally in the future.

Corporate Governance

Regarding qualitative issues concerning Nintendo I have to say there is a lot to wish for.

First of all, in the annual report there is no management discussion to speak of.

Only a small section which is called "Message of the president" or something like that. Basically it's pathetic.

Furthermore, nothing to be found regarding corporate governance or CSR (=corporate social responsibility) in the annual report. I have to admid that I have never come across an annual report in Japan having such a vacuum in that respect.

The only message regarding corporate governance is to be found on Nintendo's internet page and is stating the following:

|

| (click chart to enlarge) |

Apparently Nintendo doesn't have any independent director on their board. But three out of four auditors are independent.

Conclusion

Pros

- valuation is mouthwatering (as it is the case for soooooo many japanese corporations)

- stock is overcapatilised

- strong franchise and strong IP

- businessmodell quite easy to understand

Cons

- some accounting issues I can't get my head around

- management discussion with stockholders not existent

- pay-out policy is too complicated

- coporate governance apparently not existent

- extremely exposed to western consumers (and no Japan isn't part of the western world), which overstretched financially by any means

- stock is overcapitalised

){kind=link}

I found your blog recently and found your thesis on Nintendo interesting. I have recently started following Nintendo so I don't have much insight but your post definitely helped in furthering my understanding of the financials and business case.My main concern is corporate governance but I need to study some more to make a decision one way or the other. Thanks for the writeup.

ReplyDeleteCorporate governance is a negative, but shouldn't be a "major concern". Valuation is more important!

ReplyDeleteHi, interesting take and analysis, at your request, I will not be a silent reader! I agree and disagree. The trouble I have with Nintendo is it looks book value cheap, but the future earnings stream is very under threat from the move to smart phone gaming, cloud hosted gaming. I suspect it is overpriced at book of 1. its market share and position are probably in long term structural decline as a consequence, so a backward looking asset based valuation is potentially not fully recognising the change.

ReplyDeleteThere is a positive in that China is potentially loosening its laws on consoles, and that could be an enormous positive, given the wii's family friendly gaming environment is likely to me much more what the chinese are intending (the wii is generally not a good medium for killing people online).

Disagree that valuation is that much more important than governance when you can buy much cheaper companies that have both! A company that does not care for its shareholders (crappy yield, and cash hoard would evidence this) is not necessarily a good investment even at these levels. Poor management execution, or R&D could burn a hole in that cash very quickly. If you really believe in Nintendo, then its components suppliers (look at mitsumi, hosiden) are cash richer and price to book cheaper and far more geared to Nintendo's success from those levels. (NB I hold none of the three). Happy to debate further any time

Good points Anonymous.

ReplyDeleteAlthough not so sure about the online game competition. At least the online games the kids around me are playing (mainly when waiting or the parents watching television) look crappy to me. As soon as the telly is free they plug in the console. But really not an expert on that!

The china news came out yesterday. One has to see how this is playing out. But it would be definetly a huge plus. Also it diversify overall sales away from (financially) overstretched

western consumers.

Regarding valuation. I can't see that there is any earning power priced into the stock at the current level. Having said that, such a call is always a tricky one indeed and for sure debateable.

Furthermore, all the IP nintendo has got is not on the books!

Corporate governance for sure is always important, but I still believe that in the end it's valuation that counts most.

Totally agree competition is not there now, but it is growing and I would think combination of phone based and cloud based gaming will devour consoles long run. Its easier for consumers and that's the key. And if its easier, the shift will go there. At the moment, you need a faster delivery medium, more bandwidth, huge investment in graphics processing, but it will eventually take over. Call of duty style games stays on console for a long while, the hardcore gamers won't sacrifice until its equal or better, but if its better they will switch. Years away likely, but I see consoles in structural decline. (Another warning, Sony, a true basket case of a company rumoured to be launching PS4 this year, and if they are doing it, then consoles must be over lol). Considered nintendo for a while, because as you say, the earnings power looks free at this level. But I could not see a way for it to deliver good enough earnings long term and at the end of the day, assets are nothing if you cant make money from them, and the visibility on what it might invest in and develop is just not there with competition so fierce. It has innovated very well in the past though so it may have tricks up its sleeve still.... I suspect it is going up because it 'looks' cheap, but a PB of 1 is not necessarily cheap when you look at what you can earn from those assets, or when you look around the market. The wii u sales are ok but not great (they should grow though) and it looks like it will lose money this year. Software development and licensing is short run off business and it could hit a real earnings cliff again. they need a new killer consumer product to really drive earnings and to me the risk reward is just not there at this level. it smells more like a value trap to me. And given there are easier stocks out there to work out - PBs of 0.4-0.5, but 100%+ of the market cap in straight cash, business models that work, earnings that are growing and management that looks after shareholders - that's the place to look if you ask me.

ReplyDeleteIP in Japan is definitely a very interesting area. The Japanese - through the excesses and overinvestment of the 80s and 90s - have built a huge amount of brand and patent power... one example look at Canon, its patent portfolio (also not on the books) is vast. And management are good too, well run company.

If valuation counts most, when do you get off...? When does Nintendo stop looking G&D cheap? Why is one of its biggest suppliers, with nearly all its sales solely to nintendo much, much cheaper? Because people haven't heard of it, and everyone has heard of nintendo...

"Maybe more interesting than the WiiU console in itself for future sales might be the network strategy Nintendo is introducing with the console launch. Here especially I find the video on demand strategy quite appealing, as content is as important (or even more so) than hardware"

ReplyDeleteVery much agree. That's the key to me. Not VoD - bad business - but the Nintendo-network stuff. Perhaps small low-priced downloadable apps for kids to play with their friends. As I mentioned before, the wii is not a good environment for killing people, nintendo has always been family friendly. Could make a lot of money

I like your arguments about operational issues on Nintendo. Can't give you really a qualified opinion on it. I am of the opinion that "investors" in general are too much foused on P&l account when "valuing" a company. Balance sheet often entirely dismissed as being of no importance. Your arguments tend to go in the same direction. On that one I totally disagree! Balance sheet of utter importance!

ReplyDelete"Why is one of its biggest suppliers, with nearly all its sales solely to nintendo much, much cheaper? Because people haven't heard of it, and everyone has heard of nintendo..."

If you mean the suppliers you mentioned yesterday, I have to say I wasn't too impressed by the quantitive metrics!

" And given there are easier stocks out there to work out - PBs of 0.4-0.5, but 100%+ of the market cap in straight cash, business models that work, earnings that are growing and management that looks after shareholders - that's the place to look if you ask me."

Disagree. Not so easy to find those stocks!!! Wouldn't mind if you gave me an example. Mitsumi and Hosiden definetly not in that category.

And by the way.

ReplyDeleteCanon's corporate governance framework isn't any better than Nintendo's.

Not one independent director on a 19 members board.

Balance sheet first always, absolutely agree with you there. but only looking at balance sheet is too narrow, you need to take a view on what it will do with its balance sheet too. I want to understand what it does, how cash moves through the business and what will change. Otherwise a strong balance sheet can just be a cheap company going nowhere, of which there are loads in Japan.

ReplyDeleteMitsumi has 93% of its market cap in straight cash, and is on a price to book of 0.45. its a balance sheet cheap company. Its been losing money, but with that much cash it can ride out troubles. But I would not buy it due to its reliance on sales to nintendo. I was just pointing out that if nintendo is on a PB of 1, then why is one of its key suppliers less than half of that? If nintendo succeeds, mitsumi has much more operational gearing to its success than nintendo does and so I would own mitsumi before nintendo.

Also - dont really look at corporate governance in that way - I meant governance in the sense of how the company is run. Dont really care about independent directors etc as Japan works in a different way, you can have all the independents you like, if the chairman or family owns a big chunk of the company they founded, independents dont matter. I mean is it well governed in the sense that are they going do right by me as a shareholder and make me money and return me money. Canon yields nearly 4%, its bought back stacks of its own shares, the management is honest and executes its plans effectively. That's caring about shareholders. I dont own Canon, but its a good company.

I'm afraid I can't share names of what I hold, have a duty to paying clients (but you are correct in that they are not so easy to find... just they are easier businesses to work out than nintendo! But we have plenty of them and there are lots still out there...). But always happy to argue about things that I dont hold. I will not be a silent reader! Your blog is interesting and you have some good stuff on here. Thank you

(part one)

ReplyDeleteFirst of all thanks for the kudos.

Your comments are very much appreciated and I think they do add to the quality of that post.

"Balance sheet first always, absolutely agree with you there. but only looking at balance sheet is too narrow, you need to take a view on what it will do with its balance sheet too. I want to understand what it does, how cash moves through the business and what will change. Otherwise a strong balance sheet can just be a cheap company going nowhere, of which there are loads in Japan. "

I didn't mean to say that future earning power isn't of importance! It is of utter importance. And I do try to get my head around some rudimentary question concerning that issue. But I am much aware of the fact, that one can get on a slippery slope easily here. I am not that megalomaniacal, that I think I can beat the "financial analysts" in the city, new york, tokyo, etc. on that game! I see my "circle of competence" in "tedious" security analysis. Digging the numbers. Trying to find hidden assets! Old school Walter Schloss, Benjamin Graham style. Not too many competition there!

Furthermore, income statements in Japan are very flawed. I have written extensively on this blog touching on that matter!

"Mitsumi has 93% of its market cap in straight cash, and is on a price to book of 0.45. its a balance sheet cheap company. Its been losing money, but with that much cash it can ride out troubles. But I would not buy it due to its reliance on sales to nintendo. I was just pointing out that if nintendo is on a PB of 1, then why is one of its key suppliers less than half of that? If nintendo succeeds, mitsumi has much more operational gearing to its success than nintendo does and so I would own mitsumi before nintendo."

I tell you why (as far as I can see it). Firstly, Nintendo isn't (generally) making its money with the hardware! I mean Mario bros, Zelda, Pokemon, all those characters are as well known as Micky Mouse. And they start monetising on it with muppets, mainly produced by banpresto. That's only one way they can monetise on those IP. You mentioned another one, by offering it online for (cheap) downloads. I do know that the management stronlgy opposes to that strategy. I don't know why and if they are right (on the long run).

Secondly, the business is extremely capex light (compared to Mitsumi).

Last but not least, they are personal light. I mean it is quite impressing how much sales per employee they manage(d) to generate (in average). Mitsui is totally the opposite.

Conclusion: One could argue that buying into a software/ toy manufacturer :-) that is exposed to Nintendo could be more promising.

Having said that, for sure operational leverage would be much higher with mitsumi. But unfortunately that comes with a lot of operational risk. And I hate risk and leverage!

(part two)

ReplyDelete"Also - dont really look at corporate governance in that way - I meant governance in the sense of how the company is run. Dont really care about independent directors etc as Japan works in a different way, you can have all the independents you like, if the chairman or family owns a big chunk of the company they founded, independents dont matter. I mean is it well governed in the sense that are they going do right by me as a shareholder and make me money and return me money. Canon yields nearly 4%, its bought back stacks of its own shares, the management is honest and executes its plans effectively. That's caring about shareholders. I dont own Canon, but its a good company."

Yeah got it. Basically I am with you on that one. But it is a major plus if the governance framework supports your observations. If you have read my other posts on individual stocks you'll see that I regard payout (dividend+share buyback) to shareholders as utterly important, when deciding to buy into a holding.

"I'm afraid I can't share names of what I hold, have a duty to paying clients (but you are correct in that they are not so easy to find... "

You could contact me privately :-) Not going to publish them.

Anyways

Greetings

My fault for only stumbling upon you recently... I have not read the back history. I think the first one was Japan's real trade balance which was oh so true. I think I have misunderstood you and we definitely agree on a lot of things.

ReplyDeleteTrouble is, Nintendo will still waste money developing hardware. You can bet on that. Just like Sony will still waste money developing bigger and more expensive TVs with ever more features that people dont want or need. Neither are good investments in current form. (I could rant at length about sony... if it just stopped wasting money making TVs it would make lots of money. But it never will). And as for panasonic... your point about #employees very valid. Off top of my head Sony has about 170,000, Panasonic about 350,000. LG Electronics about 35,000, all broadly similar market cap...

Dont use blogs a lot and cant find how to contact you privately. No link in the profile?

Contact buttom in the header (under the headline undervaluedjapan).

ReplyDeleteAlso you can write a comment with your email. Won't publish it and contact you!

Did a post on Sony last year.

ReplyDeletehttp://undervaluedjapan.blogspot.de/2012/06/disturbing-sony-jp6758.html

I do like their tellies though :). But yeah bad business. As far as I can see it most of their profits come from the insurance business.

But not following sony really. Most interested in domestic value stocks.