Introduction

Fukuda Denshi was first presented on the blog in 2012. Since mentioning the company the stock price has more than trippled.

In this post I will make the case that Fukuda Denshi is a wonderful company that, irrespectively of the significant share price appreciation, is still a bargain issue.

Company and Market Overview

Company Overview

Fukuda Denshi Co, Ltd. is a

manufacturer of medical electronics equipment, having strengths in those

related to the cardiovascular system. The company was founded in 1948 and

developed the first electrocardiograph in Japan.

Fukuda Denshi is mainly focused on the

Japanese medical device market and has little international presence. It offers

a wide range of medical equipment products. Among other products, like software

and ultrasound paper, it offers defibrillators, patient monitoring - (central

and bedside), vascular screening -, ultrasound -, stress test - and respiratory

systems. In addition, the company provides therapeutic instruments for sleep

apnea syndrome and sells AED (automated external defibrillators) made by

Philips for cardiopulmonary resuscitation.

Lately, the company is making efforts

on expanding its lineup for rental medical equipment for home care, including

oxygen concentrator devices.

Market Overview

The medical device market is a segment

of the Japanese economy that has been showing satisfactory organic growth in

recent years. Due to the aging society it is expected to continue to expand in

the foreseeable future.

But the growth of the medical device market segment in Japan is not as spectacular as in other regions, like the USA. The main driver of the subdued trend is the strict cost control the Japanese adhere to when it comes to healthcare spending. It manifest itself in a relatively small health expenditure per capita (see graph), as well as in relation to the GDP. In 2011, for example, Japan’s expenditure for the healthcare system was roughly 9% of its GDP. Just a fraction of the 18 % recorded in the USA.

Analysis of Operation, Cash Flow and Balance Sheet

Analysis of Operation

Over a time frame of 17 years Fukuda

Denshi was able to grow its turnover by roughly 3, 6% p.a., and thus, can be

viewed as moderately growing.

The financial crisis of 2008/2009 had

no negative influence on Fukuda’s turnover and/ or operating margins. Neither

did the fragile state of the Japanese economy in the aftermath.

This operational stability in

turbulent times shows impressively the defensive nature of the

market segment in which Fukuda Denshi operates. In addition, does it exemplify

that the company is shielded from the vagaries of the Forex market. On one

hand, because Fukuda Denshi is almost exclusively focused on the domestic

market. On the other hand, because the company running a division that is

dependent on imports of third party products from overseas suppliers. Hence, a

rising yen lowers procurement costs and contributes positively to operating

margins.

The stable/ expanding operating margins

of the post crisis years stand in stark contrast to severe pressure on them in

the pre- crisis era. The margin pressure between 2001-2005 was mainly due to an

increasingly conservative accounting policy in combination with a weaker yen.

Whereas, the outright collapse between 2005/ 2006 was induced by a disposal and

extraordinary write down on a wholly owned subsidiary (Kontron SAS). It had

been purchased in 2005 and was already disposed of in 2006 at a significant

loss.

The EPS growth has outpaced the expansion of operating metrics by a wide margin. This is mainly due to significant share repurchases between 2010 and 2014 at extremely favorable terms (see pay- out policy). Return metrics expanded significantly too. But, in recent years it has not been able to keep pace with the EPS expansion, mainly due to BPS increasing faster than EPS.

The EPS growth has outpaced the expansion of operating metrics by a wide margin. This is mainly due to significant share repurchases between 2010 and 2014 at extremely favorable terms (see pay- out policy). Return metrics expanded significantly too. But, in recent years it has not been able to keep pace with the EPS expansion, mainly due to BPS increasing faster than EPS.

Analysis of Cash Flow

The significant earnings growth is

backed by the company’s ability to generate high operating cash flow, as well as

free cash- flow. Actually, generation of operating- and free cash- flow has to

be seen as Fukuda’s strong suit. In the last 17 years Fukuda Denshi has shown

the capability to structurally increase those metrics. Especially, since the

aftermath of the financial crisis operating–, as well as free- cash- flow appear

to have established a permanently higher plateau.

Not only does the ability of

generating substantial cash- flow point to an extremely high earning’s quality,

it also can be assumed that the company has a strong competitive advantage

within Japan.

The ability to generate an ever increasing amount of FCF is impressive. Especially, against the background that Fukuda Denshi has been constantly increasing investment in growth capex, which is not even considered in this FCF examination.

Analysis of Balance Sheet

{kind=link}

The growth in BPS was with 5,5% p.a. slightly higher than

growth in net assets.

Fukuda’s asset composition is highly favorable, as the company does carry little intangibles on its balance sheet and the majority of tangible assets are highly liquid.

Actually, the company has to be regarded as overcapitalized.

It manifests itself in an ever increasing net- liquid position.

Interim Conclusion:

- Long established medical device company

- Operates in a market segment of the Japanese economy that is showing organic growth due to the aging society

- Company is modestly growing in terms of sales

- Modest sales growth translates into disproportionately high economic efficiency in terms of margin and EPS expansion and, most importantly, into the ability of generating large sums of FCF

- Balance Sheet is rock solid. Actually, the company has to be regarded as overcapitalized

Valuation

General Valuation

The stated actual P/ E and P/C ratio (14 and 8) for FY 2016

appear modest. Cyclically adjusted ratios are significantly higher (29 And 14).

Mainly due to the fact of a run up in the company’s stock price in recent

years in combination with subdued operational efficiency in former years.

As noted above, stated operating margins and return metrics

are satisfactory, especially when keeping in mind dealing with a Japanese

company. The structural increase of Fukuda Denshi’s operational efficiency in

recent years becomes apparent when comparing them to the average operating

margins and return metrics. The company’s average ROE and net operating margins

are 6% and 5% compared to actual readings for the FY 2016 of 8,3% and 7,2%.

At current market capitalization Fukuda Denshi’s stated P/B

ratio is slightly above 1.

All the above mentioned valuation metrics on price basis make

up for a company that is modestly valued, but not a steal. So where is the

beef?

On the flaws of Price Ratios

Well, it is to be found in the fact that price metrics can be

very misleading valuation metrics indeed, especially in Japan.

Because standard price ratios do not give away the "true" state of a companies’ valuation granted by the market.

In many instances P/ OCF and P/E overstate or understate the

valuation of a company by a wide margin. Although, widely followed and eagerly

marketed by the financial media and financial community, price metrics, at

best, do not deserve the prominent position they are granted by market pundits.

At worst they are detrimental to your wealth.

Especially the P/E ratio is the most overhyped and flawed

ratio, and dangerous as hell when taken at face value. Unlike the P/OCF ratio,

which is mainly distorted through the numerator (P), the P/E ratio can be so by

the numerator and denominator.

The distortion of the numerator mainly comes into play when

not taking into account differences in the capital structure of a company, e.g.

debt vs. equity financing. The denominator is distorted by different accounting

standards and accounting assumptions.

Making the Case for Enterprise Value

In the case for EV, the market capitalization is adjusted for

the interest bearing debt on the balance sheet (e.g. added to the market cap)

and the companies’ cash balance (e.g. subtracted from the market cap).

Basically, the EV is the money a potential buyer has to put up for acquiring

the whole company at prevailing market prices.

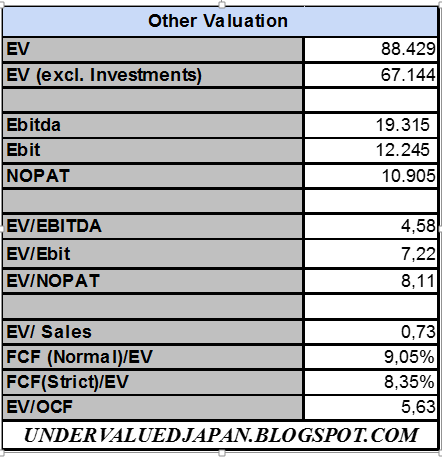

In Fukuda Denshi’s case the following valuation picture

emerges following the analytical concept of EV.

With an EV/Ebit ratio of 7 and EV/OCF of 6 it becomes apparent

that the company is not only moderately valued by the market, but rather cheap.

In addition, if we excluded Fukuda’s investment portfolio from our EV calculation, which is highly liquid and marked to market, the Company becomes an outright steal.

Comparative Valuation: Fukuda

Denshi vs. Nihon Kohden

Fukuda Denshi’s main competitor on the Japanese market is the company Nihon Kohden. Thus, it lend itself to perform a comparative analysis of these two companies.

Already when comparing the price metrics and operating margins of those two companies, the value discrepancy becomes apparent. Although exhibiting almost the same operational efficiency, Fukuda Denshi is trading at a significant discount to Nihon. In addition, does Fukuda Denshi offer a significant better dividend yield.

But how steep Fukuda Denshi’s relative discount really is

becomes only apparent with a comparative analysis on EV basis.

Whatever EV ratio you take into account, they all show that Fukuda Denshi trades only at a fraction of Nihon Kohden. And this for the company that has the higher Roic (ex. Cash and marketable securities) and FCF yield!

Whatever EV ratio you take into account, they all show that Fukuda Denshi trades only at a fraction of Nihon Kohden. And this for the company that has the higher Roic (ex. Cash and marketable securities) and FCF yield!

In addition, when taking Fukuda Denshi’s significant investment

portfolio into account the valuation discrepancy of those two companies become

outright obscene.

Intrinsic

Value

Certainly, Fukuda Denshi is not such a deep value bargain

issue like in 2012 when I first mentioned the stock on this blog at around 2500

Yen,

Nevertheless, it is my conviction that Fukuda Denshi still

offers a lot of intrinsic value in relation to the prevailing market price on

several counts.

Fukuda’s NCAV stands at roughly 5000 Yen per share and is

increasing significantly over time. Thus, at the time of writing one pays only

1,6 times the NCAV. For such a high quality stock I would regard the NCAV value

the floor in the absolute worst case scenario in case of a full blown market meltdown.

Concentrating solely on the asset power value, and discounting

the actual dividend into the infinite future leads to the conservative

assumption concerning Fukuda Denshi’s intrinsic value. Here the model indicates

a fair and moderately rising valuation.

The more aggressive assumption concerning Fukuda Denshi’s

intrinsic value focuses more on its earning power. This model indicates a

significantly rising intrinsic value over time and deep undervaluation of the

stock.

The total intrinsic value in the aggressive case is composed

of the following components:

Interim Conclusion:

- Price ratios do reveal the attractive valuation Fukuda Denshi is been traded at only partially

- EV analysis in combination with Ebit/ Ebitda paramount when analyzing Japanese companies, due to high net liquid asset position and conservative accounting policy

- Only EV analysis reveals attractiveness of Fukuda Denshi at current market price

- Comparative Analysis with Fukuda’s main competitor reveals the cheapness not only on an absolut basis, but also on a relative basis

- Depending on focus , i.e. assets and dividend vs. assets and earning power, Fukuda Denshi is trading around its intrinsic value or significantly below it

- Intrinsic Value is in both cases rising over time

Analysis of Pay- Out Policy

Fukuda Denshi is actually paying a dividend of 160 Yen p.a. leading to a dividend yield of roughly 2% and a stated dividend payout ratio of 25% for FY 2016.

The dividend per share doubled in the last several years. But

this was not due to a significant increase in the absolute amounts of profits

returned to the shareholders, but rather an aggressive share buy- back program

decreasing the outstanding shares significantly.

At the peak of the buyback program in 2014 outstanding shares

were reduced by almost 30%. The disposal of treasury shares in 2015 were a

result of making Atomic Sankyo a wholly owned subsidiary (see corporate

governance).

The buybacks between 2010 and 2015 were conducted at

incredibly favorable terms. That is around or significantly below book value.

Corporate Governance

When I first mentioned the stock on this blog in 2012,

corporate governance was an issue for me.

Although, the company still has a takeover defense measure in

place, a lot has changed to the positive since I first mentioned the company on

the blog in 2012.

Mainly, because the ownership structure has become much more transparent. As it turned out two entities close to the founder’s family, which were major shareholders in the company, got dismantled.

The first one was Tokyo Enterprise Co.Ltd. It sold its 7,5%

stake into the off- market share repurchase programs the company executed. The

shares could be purchased by the company at incredible low valuations.

More importantly though, Atomic Sankyo was turned into a

wholly owned subsidiary in 2015. Atomic Sankyo was a major shareholder of the

company with a 14% stake and 100% controlled by the founder’s family. It had

business relationships with Fukuda Denshi selling electrocardiogram recording

paper and renting out office space. Although, I am not aware of any improper

transactions between Fukuda Denshi and Atomic Sankyo, it is very comforting to

see that the company and Fukuda-San seemed to be aware of the intransparency of

this interconnectedness and the potential for abuse. Apparently, Atomic Sankyo

was taken over at favorable terms as negative goodwill was reported on the

transaction.

The transaction was financed by giving treasury shares to

Fukuda- San. Kotaro Fukuda is now the largest shareholder of the company

holding 17,7% of the outstanding shares.

Conclusion

- Company engaged in an attractive segment of the Japanese economy that can be expected to keep on showing organic growth in the future

- Fukuda is a mildly growing, but hugely cash generative company that is attractively valued in terms of assets, earnings and, most importantly, free cash- flow.

- Fukuda Denshi’s attractive valuation is not apparent at plain sight, i.e. by scrutinizing stated price ratios. Only when the market cap is adjusted for high cash holdings and the high investment portfolio, i.e. a valuation on enterprise value basis is conducted, does its undervaluation become apparent.

- Fukuda Denshi is also very attractively valued in comparison to its main competitor Nihon Kohden

- Given the limited international presence of the company, it must be viewed as a domestic value play.

- Pay- out policy is satisfactory. Especially the significant share repurchases between 2010-2014 at very attractive terms were value accretive on the long-run. Still, given the ability of generating significant free cash- flow and an ever increasing net liquid position in the balance sheet, in combination with an attractive valuation of the stock, more action is warranted

- Good Corporate governance is evolving, as the ownership structure has become more transparent, and the potential of conflicts of interests was mended by making Atomic Sankyo a wholly owned subsidiary

Disclaimer: Long Fukuda Denshi

: The Three Bagger Stock That Still Is a Bargain ){kind=link}

Thanks for the post. Why is EV Y88bn while Bloomberg shows Y120bn. It seems your calculation of market cap is Y125bn while Bloomberg has Y160bn. Is it due to treasury shares?

ReplyDeleteYes. Discrepancy is due to treasury shares.

Deleteyou forgot to add a Label to this blog post. thanks for sharing.

ReplyDeleteThanks

DeleteIs buybacks going to continue?

ReplyDeleteI haven't got a clue!

DeleteGreat detailed analyses, Where do you get your data from? Kaisha Shikiho?

ReplyDeleteThanks.

DeleteI've got the Japan company handbook.

But most of the data is actually coming from their english website. The englisch data is a little bit hidden.

Hey O-Tone!

ReplyDeleteThank you for the absolutely excellent write up!

Just a quick question - how and where do you find the numbers to exclude FD's investment numbers from their total EV? Thank you!

Thanks Lucas.

DeleteI don't know what you mean with FD's (I reckon foreign direct)

The Investments I exclude are mentioned in the financial reports under long- term assets. In Fukuda's case mainly listed Japanese stocks.

Under JGAAP they have to be marked to market.

Great work... as always! Much appreciated!

ReplyDeleteThanks

DeleteA "new" thesis in Value investors club mentions this company.

ReplyDeleteIt is trading at about Y7,500

Might be worth checking again.

Thanks for the informative post.

Not a member of VIC. Would you mind sharing the intrinsic value they come up with?

DeleteThey do not provide a specific figure. Anyway, I have "saved as" the page with the thesis, and uploaded it to a free server (its less than 1Mb).

ReplyDeleteThe file is a zip with a webpage (6960.html) and a folder of the same name with images and what not of the page.

Just unzip the file, and double click on the webpage. Hopefully, you can read the whole thesis then. Let me know if it doesnt work.

The link is:

https://file.io/NH53rnnotPIF

Thanks Grammaticus.

DeleteWorked perfectly fine!

this is a great write up, thanks very much. I did my own before coming across yours: https://docs.google.com/document/d/1Rm802o2P1fa6gKLwHcf49Wbu-OQN03mMCFm6o3uDyTE/edit?usp=sharing

ReplyDeleteThanks.

DeleteLiked yours too.